Update on My eToro withdrawal issue.

Update on My eToro withdrawal issue.

I got some of my money back.

Well that escalated quickly.

About an hour after my post, I received a few messages from e-Toro, including an email from the head of SEA client facing. He was very professional and immediately apologized for the experience and acknowledged their customer service shortcomings in their process, and immediately outlined the steps they will take to rectify it.

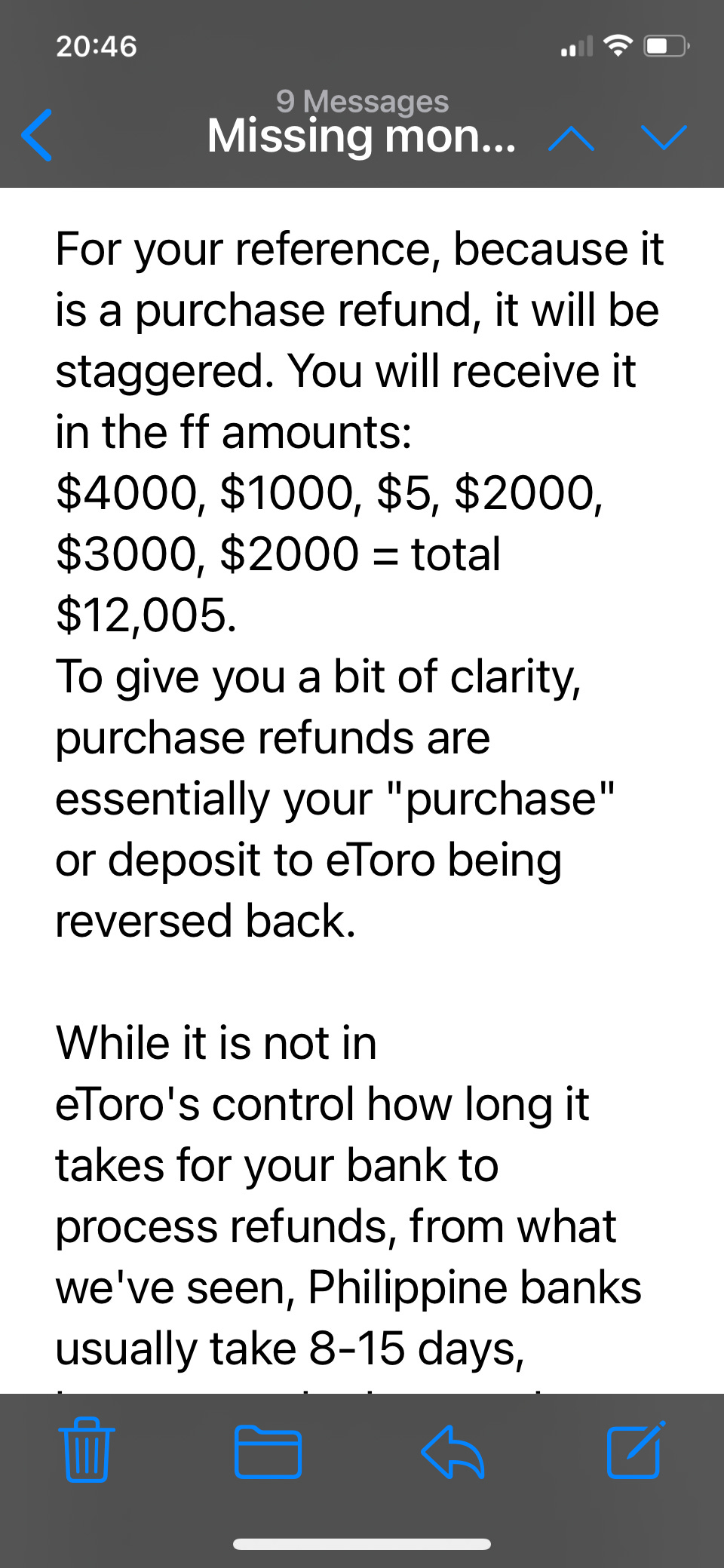

So this is the breakdown. Firstly, they transferred $940 USD into my PayPal yesterday. As of this writing, the remaining balance is still outstanding but will be transferred back into my credit card eventually in this format.

I’ll admit I chuckled to myself because parang they were asking for 6 gives, or hulugan, but turns out it’s a complicated process because funds need to go back to the source, which in this case was my overheated credit card. Hence the reason for me hitting the alarm bells after 2 weeks, because I was now paying CC interest on the amount I was owed.

Jeff, the client facing manager who took on the case, also agrees that because the source of funds never changed throughout the life of the account, it should have never reached this stage. But it did, and there are lessons here on all sides.

First lesson, regardless how tedious the process is, always read the terms and conditions. I know, I know…it’s like reading the manual for your car or new fridge, and companies really should find an easier way to communicate the key points in the sign up page as nobody reads the T&C, but ultimately, whether we like it or not, it is our responsibility as account holders to also know the process in advance.

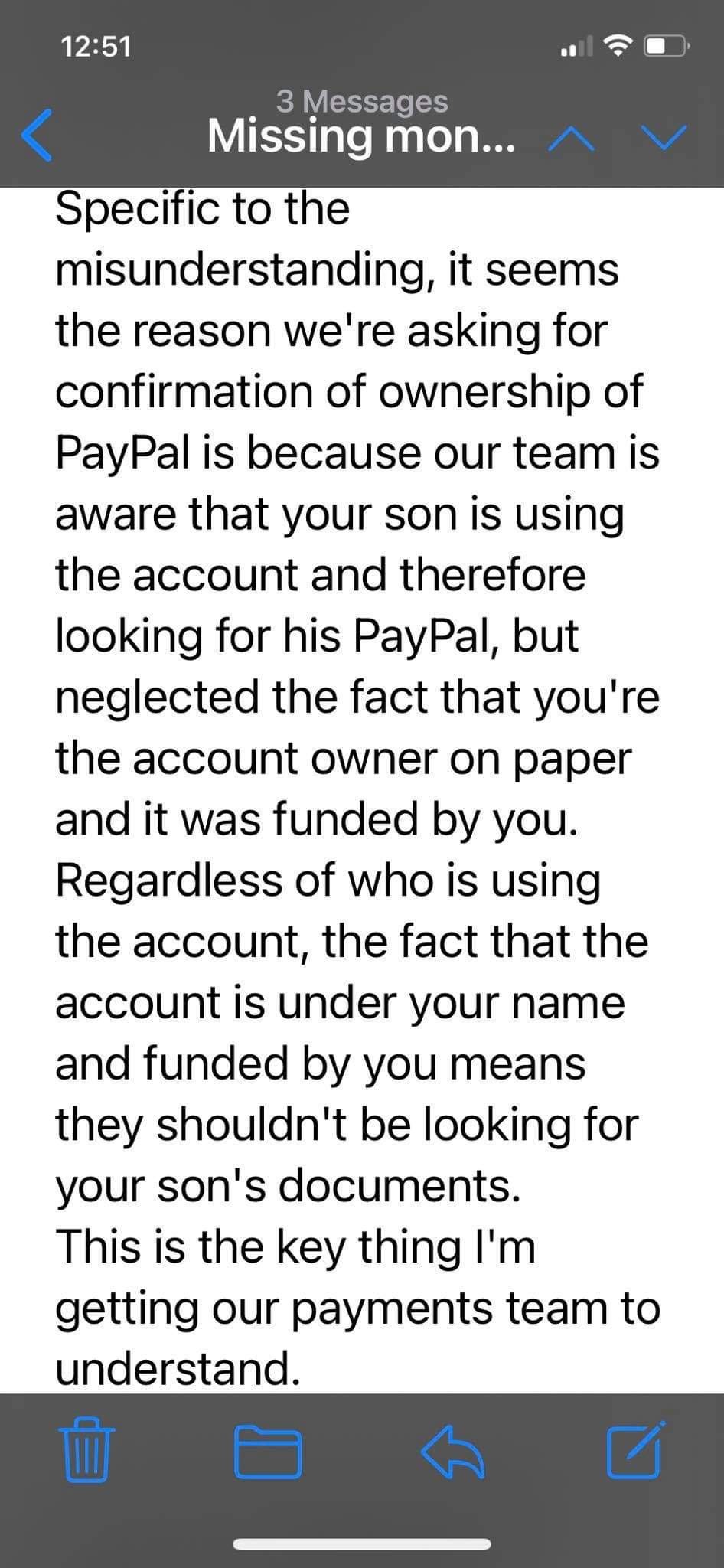

My mistake here was not doing that and sharing an account with my son. I didn’t know that was an issue––especially as most boomers in this space are being encouraged and guided by their children––but in an overly paranoid and regulated industry like finance, it’s a red flag. Period. And ignorance of the law is not a valid plea. I understand that. Yes they could have––and should have––exercised a more pragmatic approach, like flagging the deposit instead of the withdrawal (which would have avoided the whole problem from the start) but to be fair, I also have some responsibility here and I accept that.

Where e-toro and other similar apps really need to improve on though is customer communication. Especially since they are beholden to a lot of financial regulations in multiple jurisdictions that are out of their control. Because let’s face it, one hour when your money is missing can feel like one year. So you can imagine what two weeks of no answers felt like. That has to be fixed mainly because this is a business of trust. And nothing erodes that faster than silence or vagueness during a storm.

Also, because it is generally complicated and funds do take 3-20 days or so to be released even under perfect circumstances, the withdrawal process should be more prominently featured in their sign up process. Perhaps a pop up test, just like what Binance has when you enter into future trading or margins. As it is considered high risk, they require you to complete a quiz so they know that you know what you’re getting yourself into. It’s actually very effective.

So that’s my experience and outcome in a nutshell. I really hate having to go public with things like this, but I only did so after I felt I had already exhausted all channels internally. And as I said before, 2 weeks in this situation is amplified; it felt more like a decade of anxiety compressed into 14 days. So I’ll leave you with some advice, which I got from some readers, so I can at least share what I learned. This one was from a guy called Mark and I think it sums up the main points.

1. Better use a debit card and not a credit card. The eToro withdrawal rule for security purposes is that you can only withdraw from the card that you first used to invest in eToro, unless you place a note that you will use another card to receive the funds. They only allow depositing of withdrawn funds to cards that you used to fund for security purposes. If you use a credit card that would be a hassle as the money will come in as a credit card refund and you need to swipe away that money just to use it or ask for a manager’s check from the bank which can take long.

2. Make sure that the card you are using is named after you and not a joint account, eToro values security and does not want payments to be made to joint accounts because the money might be withdrawn by someone else

3. You can check the eToro withdrawal status in your account dashboard, if it says Processed it means the money has been sent to the Philippine bank, sometimes it is the PH bank who is delaying the payment (this wasn’t the case with me, but its handy to know)

4. Withdrawal is usually 3 days processing with eToro and another 5-20 days with the Philippine bank depending on what bank you use.

5. If you think email is not responsive use the chat support of eToro so you get immediate response.

6. Make small withdrawals so you can test the withdrawal process and how long it will usually take so you know the process in the future withdrawals and you can anticipate the speed of the payout

***Remember when dealing with foreign currency the payout can be slow as you are moving money from one country to another. As reference, when you issue a USD check the clearing can take as much as 30-45 days just to encash your USD check.

So there. I hope this has helped new investors out there and given eToro a few tips on how to win back the confidence of those still looking at getting into this space. Because as traumatic as the experience was, online trading, crypto, and the whole DeFi space is about to explode and is the way of the future. So the earlier you get your feet wet, the more advantages you can have when it goes totally mainstream. Personally, this has not put me off crypto or online trading. Ill be honest when I say that it may not be on e-Toro, but I can also appreciate when a company makes good on a complaint so I won’t shut that door permanently. We all make mistakes and I always believe that it’s not so much what you did or failed to do that you should be measured by, but what you do about it.

And to be fair, eToro did grab the bull by the horns in the end.

PS: I’ll post again once the credit card reversal goes through.

Hi James, the "advice" of "Mark" from the previous post is not entirely correct.

"The eToro withdrawal rule for security purposes is that you can only withdraw from the card that you first used to invest in eToro, unless you place a note that you will use another card to receive the funds."

Actually, it's not really because of security purposes. They can just request for proof of bank account if that is the case.

The real reason why they want to withdraw your funds only to the same deposit method is because of the so-called "merchant discount rate" for Visa/Mastercard credit/debit cards, or analogously the "merchant fees" for Paypal accounts. When you perform a deposit via card or Paypal, eToro actually pays a percentage of the transaction as fees to the payment processor. It can be anywhere from 1-4%. But they offer "free deposits". So if you were free to deposit with card/Paypal, then withdraw to bank, they are effectively paying for the flow of money.

By comparison, other platforms that allow debit/credit card deposits also usually charge a fee for this (e.g. GCash and Paymaya started with free card deposits, but eventually charged fees as they have been absorbing these fees initially just to help with market adoption; or the local brokerage First Metro Securities which allows debit/credit card deposits but charges 2.95% in "convenience fees"; or even Binance which also allows debit/credit card deposits, but charge the higher of 3.5% or 10 USD in "transaction fees").

But, if they issue "refunds" to your original deposits, the fees they pay to their payment processors are also refunded back to them. This is the main reason why they only allow withdrawal to the same card - so they can save on fees. Not illegal/unethical by any means, but clearly it's not just because of them "valuing security".

*There are certain cases where they can allow withdrawals to other accounts, but they require proof / bank certification that your old card/account was already closed, etc. And even then, they might insist that you simply claim the refund from the bank in case they attempt to push through with the "refund" transaction. So in these cases, it's still very burdensome, especially if your bank won't honor the crediting of the refund or cannot contact you anymore.

Glad they finally acted on returning your missing money. I can clearly see the accountability on both parties--owning up to mistakes and actually doing something to rectify the situation.